Compound Interest

Allyson Faircloth

I have chosen to do my extra write-up using #5 from Assignment 12, specifically with compound interest. This write-up is going to be a little different than my previous ones; however, I thought I would try something new. This topic caught my eye since I will soon be teaching compound interest to my senior students. I was looking for a way to get them interested in the topic. Hopefully this activity I have designed will be useful to keep them engaged while extending their knowledge of the material. However, students will have to have learned the material almost to the point of mastery to be able to complete the activity. Also, they will need to understand how to use Excel as well as have access to Excel in order to complete the following activity.

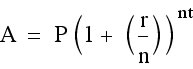

The formula for compound interest which the students will use is

where A is the total amount of money, P is the principal or starting amount, r is the decimal equivalent of the interest rate, n is the number of times the interest is compounded each year, and t is the number of years.

Activity:

1. You are looking to invest some money in a savings account. The bank you have chosen has a 1.5% interest rate per year. If you never spend any of it and never add any money to the account once the principle has been put in, how much money will you have after 50 years if you invest the following amounts of money? How much interest did you gain after 50 years?

a. $1

b. $10

c. $50

d. $100

e. $1,000

f. $10,000

2. Your friend only has $50 to invest in an account. Would it be better for him to use a bank with an interest rate of 5% for 25 years or a bank with an interest rate of 9% per year for 20 years? Why?

3. If you invest $30 in a savings account with a .95% interest rate, how long will it take you to gain $20 in interest?

4. You are managing a bank. A person comes in with $10,000 to invest in a savings account. They have already been to one bank promising them an interest rate of 3.5% per year for 25 years. Come up with your own interest rate which will allow your customer to gain about the same amount of interest in only 20 years.

5. You are looking to buy your dream car (a 2012 Corvette)! It costs $44, 890. You are going to have to set up a playment plan, and the car dealership has given you the three options shown below. Set up an excel sheet to see which plan will be the best for you. (Take into consideration the time it will take to pay off the loan and how much interest you will have to pay.)

1. $950 per month with a 2.37% monthly interest rate

2. $1300 per month with a 3.75% monthly interest rate

3. $1150 per month with a 3.24% monthly interest rate

Possible student responses for the activity:

Click here for an example Excel file for the above activity. Each problem above is on its own sheet.

1.

a) By investing $1, you would only have $2.11 in your account after 50 years. The interest that you gained would be $2.11 - $1 or $1.11.

b) By investing $10, you would only have $21.05 in your account after 50 years. The interest that you gained would be $21.05 - $10 or $11.05.

c) By investing $50, you would have $105.26 in your account after 50 years. The interest that you gained would be $105.26 - $50 or $55.26.

d) By investing $100, you would have $210.52 in your account after 50 years. The interest that you gained would be $210.52 - $100 or $110.52.

e) By investing $1000, you would have $2105.24 in your account after 50 years. The interest that you gained would be $2105.24 - $1000 or $1105.24.

f) By investing $10,000, you would have $21,052.42 in your account after 50 years. The interest that you gained would be $21,052.42 - $10,000 or $11,052.42.

2. Students will need to find the maturity value for each situation. From the spreadsheet, we see that by investing the $50 at a 5% yearly interest rate for 25 years he will end up with $169.32. That means he gained $119.32. However, if he invests the $50 at a yearly interest rate of 9% for 20 years then he will end up with $280.22. Therefore, he will gain $230.22. Thus, the better option for him would be to invest the money at a 9% interest rate for 20 years. He will gain more money in less time.

3. For this problem, we need to know when our total amount of money is $50. If our principle is $30 then a $20 gain would put the total at $50. From our spreadsheet, we see that after 54 years our total amount of money is $49.98 and after 55 years our total amount of money is $50.46. Thus, we would gain $20 shortly after 54 years.

4. In order to come up with our own interest rate, we first need to know how much interest the customer will gain by choosing the other bank. We see from our spread sheet that after 25 years our customer would have $23,632.45. They invested their $10,000 and gained $13,632.45 in interest. We can now set up our own data tables to see what interest we should offer the customers for 20 years. We can try some different numbers. By using an interest rate of .044, our customer will gain $13,659.74 or have a total of $23659.74 after 20 years. Thus, we should offer the customer a 4.4% yearly interest rate for 20 years.

5. For each of the options we will be taking out the same loan of $44,890. With option 1, we will be making the smallest payment of $950 a month. However, it will take 48 months or 4 years to pay off our loan. We will also end up paying back $355.68 in interest. For option 2, we have to make the largest payment of $1300 a month. It will take only 38 months or 3 years and 2 months to pay off the loan, but we will have to pay $445.73 in interest. Option 3 allows us to pay $1150 a month. It will take us 43 months or 3 years 7 months to pay off the loan. Also, we will have to pay the most interest of $474.76. From looking at all the data, I would have to choose the first option. I would have to make payments for a longer amount of time; however, I would pay the least amount in interest and have to make a smaller payment each month. (Students could have their own reasons for which option they would choose as long as they use the data to support their reasoning.)

*After completing this write-up, I have found that this activity will take longer than I previously imagined. This activity may have a better purpose as a final project for a unit or be broken up into parts for different lessons. It also requires a deep understanding of the topic or else students will struggle throughout the activity. However, if the students are able to complete the activity, you will know they have learned the material at a deeper level.

Return